- Sometimes, you can get a store credit card that can help build credit.

- A secured credit card also can help you build your credit.

Why is my credit report important?

Businesses look at your credit report when you apply for:

- loans from a bank

- credit cards

- jobs

- insurance

If you apply for one of these, the business wants to know if you pay your bills. The business also wants to know if you owe money to someone else. The business uses the information in your credit report to decide whether to give you a loan, a credit card, a job, or insurance.

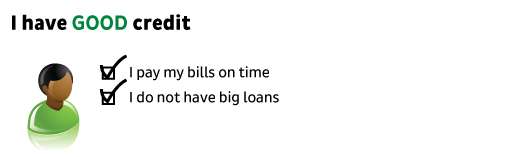

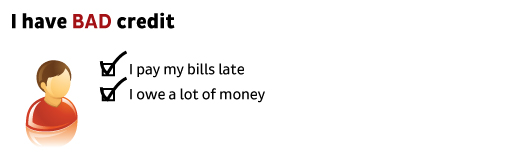

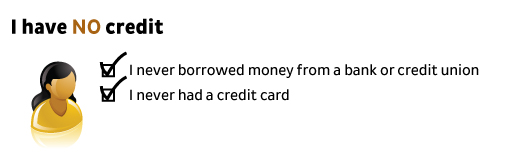

What does “good credit” mean?

Some people have good credit. Some people have bad credit. Some people do not have a credit history. Businesses see this in your credit report. Different things happen based on your credit history:

- I have more loan choices.

- It is easier to get credit cards.

- I pay lower interest rates.

- I pay less for loans and credit cards.

- I have fewer loan choices.

- It is harder to get credit cards.

- I pay higher interest rates.

- I pay more for loans and credit cards.

- I have no bank loan choices.

- It is very hard to get credit cards.

- I pay high interest rates.

- Loans and credit cards are hard to get and cost a lot.

All this information is in your credit report.

Why should I get my credit report?

An important reason to get your credit report is to find problems or mistakes and fix them:

- You might find somebody’s information in your report by mistake.

- You might find information about you from a long time ago.

- You might find accounts that are not yours. That might mean someone stole your identity.

You want to know what is in your report. The information in your report will help decide whether you get a loan, a credit card, a job or insurance.

If the information is wrong, you can try to fix it. If the information is right – but not so good – you can try to improve your credit history.

Where do I get my free credit report?

You can get your free credit report from Annual Credit Report. That is the only free place to get your report. You can get it online: AnnualCreditReport.com, or by phone: 1-877-322-8228.

You get one free report from each credit reporting company every year. That means you get three reports each year.

What should I do when I get my credit report?

Your credit report has a lot of information. Check to see if the information is correct. Is it your name and address? Do you recognize the accounts listed?

If there is wrong information in your report, try to fix it. You can write to the credit reporting company. Ask them to change the information that is wrong. You might need to send proof that the information is wrong – for example, a copy of a bill that shows the correct information. The credit reporting company must check it out and write back to you.

How do I improve my credit?

Look at your free credit report. The report will tell you how to improve your credit history. Only you can improve your credit. No one else can fix information in your credit report that is not good, but is correct.

It takes time to improve your credit history. Here are some ways to help rebuild your credit.

- Pay your bills by the date they are due. This is the most important thing you can do.

- Lower the amount you owe, especially on your credit cards. Owing a lot of money hurts your credit history.

- Do not get new credit cards if you do not need them. A lot of new credit hurts your credit history.

- Do not close older credit cards. Having credit for a longer time helps your rating.

After six to nine months of this, check your credit report again. You can use one of your free reports from Annual Credit Report.

How does a credit score work?

Your credit score is a number related to your credit history. If your credit score is high, your credit is good. If your credit score is low, your credit is bad.

There are different credit scores. Each credit reporting company creates a credit score. Other companies create scores, too. The range is different, but it usually goes from about 300 (low) to 850 (high).

It costs money to look at your credit score. Sometimes a company might say the score is free. But usually there is a cost.

What goes into a credit score?

Each company has its own way to calculate your credit score. They look at:

- how many loans and credit cards you have

- how much money you owe

- how long you have had credit

- how much new credit you have

They look at the information in your credit report and give it a number. That is your credit score.

It is very important to know what is in your credit report. If your report is good, your score will be good. You can decide if it is worth paying money to see what number someone gives your credit history.